Did you know that your credit utilization ratio makes up 30% of your credit score?

A high credit utilization ratio can lower your credit score, making it harder to get approved for loans, credit cards, or better interest rates.

The good news? Lowering your credit utilization ratio is one of the fastest ways to boost your score!

In this guide, we’ll explain what credit utilization is, why it matters, and how to lower it quickly to improve your credit score.

1. What Is Credit Utilization?

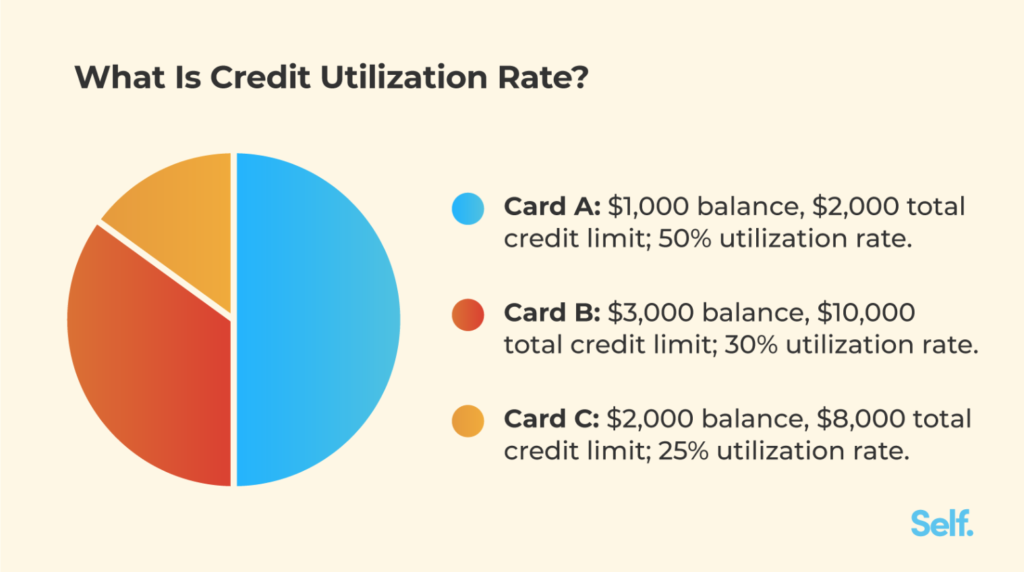

Your credit utilization ratio is the percentage of your total available credit that you’re using.

📌 Formula:

Credit Utilization = (Total Credit Card Balances ÷ Total Credit Limit) × 100

🔹 Example 1 (Good Utilization):

- Total Credit Limit: $10,000

- Total Credit Card Balance: $2,000

- Credit Utilization: 20% (Good!)

🔹 Example 2 (Bad Utilization):

- Total Credit Limit: $5,000

- Total Credit Card Balance: $4,500

- Credit Utilization: 90% (Bad!)

👉 Pro Tip: Keeping your utilization below 30% is ideal, but below 10% is even better for the best credit score boost!

2. Why Credit Utilization Affects Your Credit Score

Lenders view high credit utilization as a risk, because it may signal financial trouble.

📌 How It Impacts Your Score:

🔹 Utilization over 30%? Your score may drop.

🔹 Utilization under 10%? Your score may increase.

🔹 Maxing out a card? Your score could drop 50+ points.

👉 Pro Tip: Lowering your credit utilization can improve your score in as little as 30 days!

3. 7 Proven Ways to Lower Your Credit Utilization Fast

✅ 1. Pay Down Your Credit Card Balances

The fastest way to lower your credit utilization is to reduce your balances.

✔️ Focus on high-interest debt first (Debt Avalanche Method).

✔️ Make extra payments each month to reduce balances faster.

✔️ Use windfalls like tax refunds to pay off debt.

👉 Pro Tip: Even paying an extra $50–$100 per month can lower your utilization and boost your score.

✅ 2. Request a Credit Limit Increase

A higher credit limit instantly lowers your utilization ratio—as long as you don’t increase your spending.

✔️ Call your credit card company and request a credit limit increase.

✔️ Some issuers allow you to request it online with no hard inquiry.

✔️ If approved, your utilization drops instantly without paying off debt!

🔹 Example:

- Credit Limit: $5,000 → $7,500 (increase)

- Balance: $2,000

- Utilization: Drops from 40% to 26% → Score boost!

👉 Pro Tip: Some banks automatically increase your credit limit after 6–12 months of on-time payments—so always pay on time!

✅ 3. Spread Balances Across Multiple Cards

If one card is maxed out but others have available credit, spread your balances to reduce utilization on a single card.

✔️ Transfer part of your balance to another card with a lower balance.

✔️ Keep each card’s utilization below 30% for better impact.

👉 Pro Tip: Lenders also look at individual card utilization—so avoid maxing out any single card.

✅ 4. Pay Your Bill Before the Statement Date

Your credit card reports your balance to the credit bureaus on your statement closing date—not your due date.

✔️ If you pay early, a lower balance gets reported.

✔️ This reduces your utilization and improves your score faster.

👉 Pro Tip: Make two payments per month (one before the statement closes and another before the due date) to keep utilization low.

✅ 5. Open a New Credit Card (With Caution!)

Opening a new credit card increases your total available credit, lowering your utilization ratio.

✔️ Look for low or no annual fee cards.

✔️ Only open a new card if necessary—too many hard inquiries can hurt your score temporarily.

🔹 Example:

- Credit Limit: $5,000

- New Card Credit Limit: $3,000

- Total Available Credit: Increases to $8,000 → Utilization drops!

👉 Pro Tip: This strategy only works if you don’t add new debt!

✅ 6. Consider a Balance Transfer Card

A balance transfer card lets you move debt to a card with 0% APR for 12–18 months, helping you pay off debt faster and lower utilization.

✔️ Choose a card with 0% interest for the longest time possible.

✔️ Make aggressive payments to clear the debt before the intro rate ends.

👉 Pro Tip: Avoid balance transfers if they charge high transfer fees (3–5% of the amount transferred).

✅ 7. Avoid Closing Old Credit Cards

Closing an old credit card reduces your total available credit, which increases your utilization ratio and can lower your score.

✔️ Keep old accounts open even if you don’t use them (unless they have high fees).

✔️ Use them for small recurring charges to keep them active.

🔹 Example:

- Credit Limit: $10,000

- Close a card with a $3,000 limit → New total credit limit: $7,000

- Utilization jumps up, lowering your score.

👉 Pro Tip: If you must close a card, pay down other balances first to offset the credit limit drop.

4. How Quickly Will My Credit Score Improve?

Lowering your credit utilization ratio can boost your score in as little as 30 days.

📈 Here’s What to Expect:

✔️ First 30 days – Small improvements if balances decrease.

✔️ 3–6 months – Noticeable increase if you stay below 30% utilization.

✔️ 1 year+ – Stronger credit score, especially if you keep utilization under 10%.

👉 Pro Tip: The lower your utilization, the faster your credit score recovers!

Final Thoughts: Keep Your Credit Utilization Low for a Better Score

Lowering your credit utilization is one of the fastest and easiest ways to improve your credit score. By keeping your balances low, paying on time, and using smart strategies, you’ll boost your score and qualify for better financial opportunities.

🎯 Quick Recap:

✅ Keep credit utilization below 30% (ideally under 10%).

✅ Pay down balances as quickly as possible.

✅ Request a credit limit increase to lower utilization instantly.

✅ Make early payments before your statement closes.

✅ Keep old credit cards open to maintain a higher available credit limit.

📞 Need help improving your credit? Contact Credit Restore Lab for a FREE consultation today!

CreditRepair #LowerCreditUtilization #CreditScoreBoost #FixCreditScore #FinancialHealth #CreditLimitIncrease #DebtManagement #RebuildCredit #ImproveCreditScore #CreditEducation