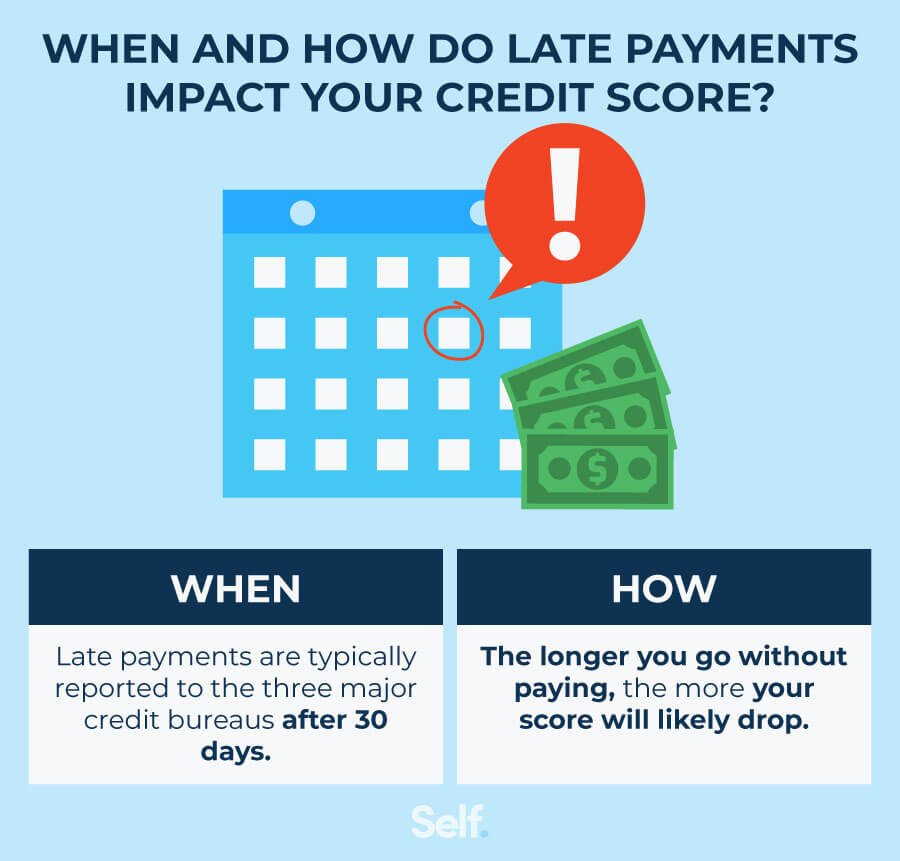

Late payments can seriously damage your credit score. Just one missed payment can cause a drop of 50–100 points, making it harder to qualify for loans, credit cards, and lower interest rates.

The good news? Late payments don’t have to haunt your credit forever!

In this guide, we’ll explain how late payments affect your credit score and the best ways to remove them from your report.

1. How Late Payments Affect Your Credit Score

Your payment history makes up 35% of your credit score, making it the most important factor.

📉 What Happens When You Miss a Payment?

🔹 1–30 days late – Usually no major impact if paid quickly.

🔹 31–60 days late – Reported to credit bureaus, causing a score drop.

🔹 61–90 days late – Bigger impact; lenders may close accounts.

🔹 90+ days late – Severe damage; account may go to collections.

👉 Pro Tip: The longer a payment is overdue, the worse the impact on your score.

2. How Much Can a Late Payment Lower Your Credit Score?

The exact impact depends on your credit history and the severity of the late payment.

📌 For a 700+ credit score: A single late payment can drop your score 50–100 points!

📌 For a lower credit score: The drop might be less severe, but it still hurts.

👉 Pro Tip: The older the late payment, the less impact it has on your score.

3. How Long Do Late Payments Stay on Your Credit Report?

- Late payments stay on your credit report for 7 years.

- However, their impact decreases over time.

- The best way to recover is to make on-time payments consistently.

👉 Pro Tip: Removing late payments from your report can boost your score fast!

4. How to Remove Late Payments from Your Credit Report

✅ 1. Ask for a Goodwill Adjustment (Best for One-Time Late Payments)

Many lenders forgive a late payment if you have a good history.

📩 How to request a goodwill removal:

- Write a Goodwill Letter to your lender.

- Explain why you were late (e.g., medical emergency, financial hardship).

- Show that you’ve been a responsible borrower otherwise.

👉 Pro Tip: Some lenders may remove the late payment as a courtesy!

✅ 2. Dispute Incorrect Late Payments

If you believe a late payment is reported in error, you can dispute it with the credit bureaus.

📌 Steps to dispute:

- Get a free credit report at AnnualCreditReport.com.

- Check for incorrect late payments.

- Submit a dispute online with Equifax, Experian, or TransUnion.

- Provide proof of payment (bank statements, confirmations).

👉 Pro Tip: If the lender can’t verify the late payment, it must be removed!

✅ 3. Negotiate a “Pay for Delete” Agreement

If your account is seriously delinquent or in collections, you may be able to negotiate removal.

📌 Steps to request “Pay for Delete”

- Call the creditor or collection agency.

- Offer to pay the debt in exchange for removing the late payment from your report.

- Get the agreement in writing before making a payment.

👉 Pro Tip: Not all lenders offer this, but it’s worth trying!

✅ 4. Wait It Out (If Other Methods Don’t Work)

If the late payment is legitimate, it will eventually disappear after 7 years.

📌 How to minimize the damage:

✔️ Continue paying on time to rebuild your score.

✔️ Keep credit card balances low to offset the impact.

✔️ Consider becoming an authorized user on someone else’s credit card to add positive history.

👉 Pro Tip: As time passes, late payments affect your score less and less.

5.Take Control of Your Credit Score

Late payments can feel like a credit score disaster, but they don’t have to be permanent.

🎯 Quick Recap:

✅ One missed payment can drop your score by 50-100 points.

✅ Late payments stay on your report for 7 years but have less impact over time.

✅ Goodwill letters, disputes, and negotiations can help remove them faster.

📞 Need help fixing your credit? Contact Credit Restore Lab for a FREE consultation today!

CreditRepair #LatePayments #FixCreditScore #IncreaseCreditScore #RemoveLatePayments #CreditScoreBoost #CreditDisputes #CreditReportErrors #ImproveCreditScore #FinancialHealth #DebtManagement #RebuildCredit #CreditRepairServices #RaiseCreditScore #CreditEducation #BadCreditFix